Exploiting a construction boom

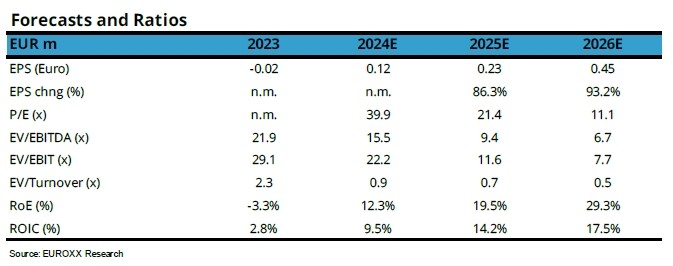

We initiate coverage on Intrakat, Greece’s second largest construction company with an Overweight Rating and a Price Target (PT) of EUR 6.4/share. Intrakat has been in a restructuring exercise over the past two years but is now ready to exploit the growth in the construction space. This turnaround will be evident in profitability over the next three years with EBITDA in 2026E reaching EUR 180m, on our numbers, from just EUR 16m in 2023.

Ready to capture the benefits of a construction boom. The Greek construction sector has already started recovering after the massive decline during the Greek crisis. This is evident by the strong growth in backlog and the project pipeline ahead. We think that Intrakat is now ready to capture this growth and we expect new orders of >EUR 10bn

over the next three years on top of the current EUR 4.9bn backlog. This should lead to turnover of c.EUR 2.4bn in 2026E (from c.EUR 850m proforma in 2023), EBITDA of EUR 180m and a ROE of c.30%.

Construction free cash flow to be reinvested in PPPs and RES. In the 2024-27E period we expect strong free cash flow generation from the construction segment with an EBITDA generation over the next four years of over EUR 500m with limited working capital needs and maintenance cap-ex in the EUR 20-40m range. This construction cash

flow will be re-invested in PPPs (private-public partnerships), concessions and renewable projects (RES). Management expects the EBITDA from PPPs to reach EUR 44m from 2030E onwards and it aims at a long term

portfolio mix of 40% construction, 30% PPPs and 30% RES.